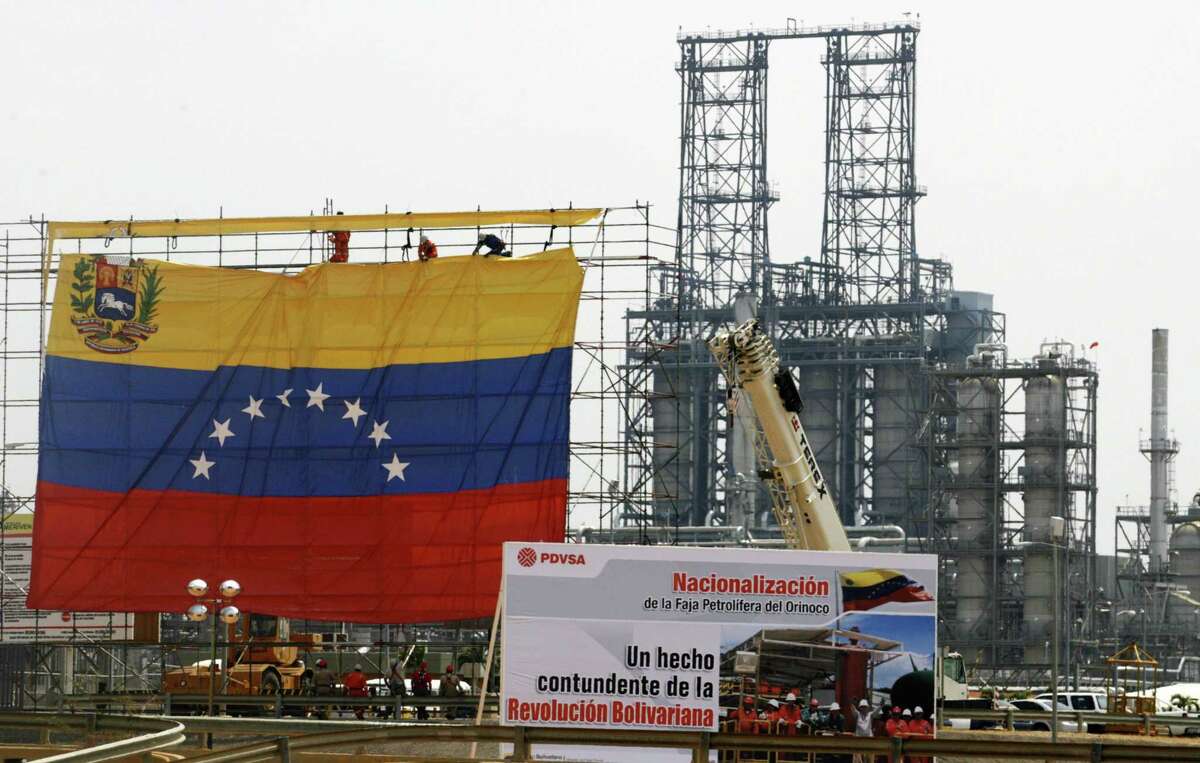

Venezuela hit a seven-year export high in May 2026, shipping 1.25 million barrels per day — a 61% year-on-year surge. The comeback is being framed as a recovery story for state oil company PDVSA, but behind the record numbers lies not Venezuelan sovereignty — it's a Washington-engineered regime change and a deliberate transfer of control over oil flows to American and Western traders.

What This Story Is Really About

On January 3, 2026, U.S. special forces conducted an operation in Caracas. Nicolás Maduro was seized and transported to the United States, where he has faced trial since January 5 on narcotrafficking charges. Acting President Delcy Rodríguez formally heads the government, while real power is shared between military strongmen Padrino and Cabello. In March, Washington officially recognized the new administration — and immediately opened the oil spigot.

Vice President Vance laid out the terms bluntly: "You are permitted to sell oil only insofar as you serve America's national interests." The flow-management architecture runs through three companies — Chevron, Vitol, and Trafigura — which collectively control the bulk of Venezuelan exports. PDVSA, in turn, is required to spend its oil revenues predominantly on American goods.

How the Buyer Map Has Changed

The reorientation of flows has been swift and stark. Before January 2026, China was Venezuela's largest oil customer. By May, the picture had fundamentally shifted: the United States took the top spot at 558,000 b/d, India ramped up purchases to 427,000 b/d, and Europe receives approximately 169,000 b/d. China, meanwhile, has slashed its intake to minimal volumes.

This is not a market-driven realignment. It is a managed redistribution: Washington is simultaneously plugging the supply gap triggered by the Hormuz crisis and systematically squeezing China out of a key heavy crude source that Beijing had spent years cultivating.

What This Means for Russia

For Russian crude exporters, Venezuela's return creates direct competition on key Asian markets. India — which had been steadily expanding Russian oil purchases at a discount since 2022 — is now simultaneously scaling up Venezuelan imports, free of sanctions exposure and backed by American political cover. Competing against that kind of offer on price alone is becoming increasingly untenable.

Venezuela's production ceiling remains constrained by crumbling infrastructure: credible estimates put the investment required for full sector recovery at $100 billion or more. That gives Russia a window of three to five years — no longer. The structural threat on Asian markets has already taken shape.

Where the Configuration Is Heading

Venezuela has become an instrument of American energy policy on two simultaneous tracks: tactically, it fills the Hormuz-driven supply deficit in Asian and European markets; strategically, it blocks China and Russia from accessing cheap Western Hemisphere crude. Washington has secured a manageable asset without the costs of sanctions. The Rodríguez government gets revenues and survival. Chevron, Vitol, and Trafigura get the margin. The losers in this configuration are China, which has lost a reliable supply channel, and Russia, which has gained a new competitor on its most important markets.

What to Do

For Russian oil exporters, the India strategy demands immediate reassessment: a discount ceases to be a sufficient competitive argument when the buyer has an alternative backed by Washington. Diversification toward Southeast Asia and Africa is no longer an option — it is a necessity. Watch Venezuela's monthly export data as a leading indicator: the pace of PDVSA's recovery will reveal the real timeline of competitive pressure on Russia's market position before any official statements do.

.png)